Filing a siding insurance claim

Storm damage can leave you stressed and unsure what to do first. A siding insurance claim may help with covered damage, but the process can feel confusing. This guide explains how to document damage, talk with the adjuster, compare repair vs. replacement, and avoid high-pressure deals.

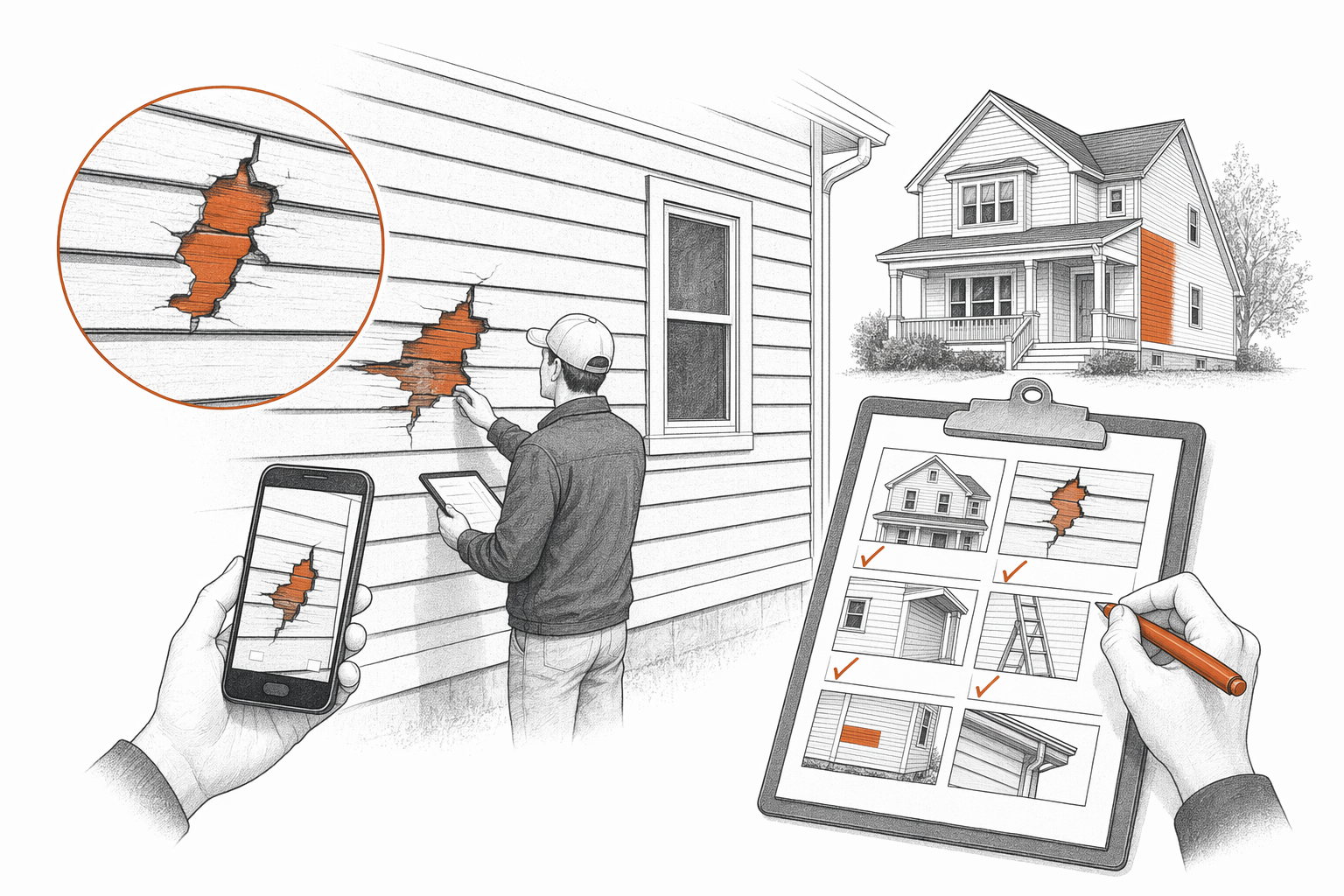

Start calm and document everything

If hail, wind, or flying debris damaged your siding, do not rush into a contract the same day. Take a breath and start with clear records. Good photos, dates, and notes can help support your claim.

A siding insurance claim is about showing what happened, when it happened, and what damage is present now. Coverage depends on your policy and the insurance company’s review. Some claims are approved for spot repairs. Others may cover a larger replacement if matching is not possible or if damage is widespread.

If you are early in the process, it can also help to review typical siding costs so you understand the size of the project. If you want to compare local pros, SidingLedger can help you get matched with licensed, insured, and bonded siding contractors near you at no cost.

Key points to know before you file

Insurance claims move more smoothly when you stay organized and keep communication in writing when possible.

Your insurer may send an adjuster to review the home. The adjuster works for the insurance side of the claim process. You can also ask licensed siding contractors to provide written findings and scope notes, but make sure they do not pressure you to sign before you are ready.

Real project pricing is not one fixed number. Siding work is usually discussed in typical per-square-foot ranges and estimates, not guarantees. Your final price depends on home size and height, material, removal of old siding, site conditions, and your area.

What to do: step by step

1. Make the area safe first. If loose pieces are hanging or water may get in, take reasonable temporary steps to reduce further damage. Keep receipts for emergency protection if your policy may require documentation.

2. Document the damage well. Take photos and video of dents, cracks, chips, lifted panels, broken trim, and any interior signs of moisture that appeared after the storm. Include wide shots of the whole exterior and close-ups with date stamps if available.

3. Review your policy basics. Look for your deductible, storm coverage language, exclusions, and deadlines for reporting. If you do not understand the wording, ask your insurer to explain it in plain language.

4. File the claim promptly. Give the insurer the date of loss, your contact information, and a simple description of what happened. Keep notes of every call: date, time, name, and what was said.

5. Meet the adjuster prepared. Have your photos, notes, and a list of visible damage areas ready. Walk around the home carefully and ask questions. You can ask what was documented, whether all elevations were reviewed, and whether matching issues were considered.

6. Get written contractor estimates. Ask local contractors for written scope and pricing. Compare line items like tear-off, disposal, house wrap or moisture barrier, trim, soffit/fascia work, and the exact siding type. Use this guide to vet a siding contractor before signing anything.

7. Compare repair vs. replacement. Sometimes repair is enough. Sometimes replacement makes more sense if damage is spread out, water intrusion is a concern, or old siding cannot be matched well. You can read more about materials and repair options in our siding repair service guide.

8. Review the insurance scope carefully. Check whether the approved scope matches the actual damage and the contractor’s written findings. If something seems missing, ask the insurer how to submit additional documentation.

9. Get the contract in writing before any deposit. The contract should list materials, quantities, prep work, cleanup, warranty details, payment schedule, and who handles permits if needed. Follow local permit and code rules.

10. Choose carefully, not quickly. If you want help comparing local companies, SidingLedger can help you get matched with licensed, insured, and bonded siding contractors near you. Verify credentials yourself before moving forward.

Common mistakes that can hurt your claim or your project

Next step: compare written scopes and choose a qualified pro

A siding insurance claim can help after real storm damage, but the claim itself does not choose the right contractor for you. Take time to compare written scopes, ask questions, and confirm credentials yourself.

Remember: prices are estimates, not guarantees. The real cost depends on home size and height, material, removal of old siding, site conditions, and your area. Before you pay a deposit, get the full scope and payment terms in writing, verify license, insurance, and bond, and make sure local permit and code requirements are followed.

If you want a simple place to start, SidingLedger is a free matching service. We can help connect you with local siding contractors so you can compare options with less stress.

After a storm, take photos, file your claim, and keep all notes in one place. Do not let anyone pressure you to sign fast. Compare written scopes, verify license, insurance, and bond yourself, and get the full job details in writing before you pay a deposit.